Ultimate Health Insurance Guide for American Indians and Alaska Natives

As an American Indian or Alaska Native (AI/AN), you may already have access to free health care through Indian Health Services, Tribal Health Providers, or Urban Indian Health Programs. Collectively, these three different types of health services are known as I/T/U. Unfortunately, these health services oftentimes can be at facilities that are far away and offer limited care, which means you may be left paying out-of-pocket for necessary treatments or specialist visits elsewhere.

This is where health insurance comes in. As an AI/AN, you are likely eligible for low-cost (or free!) health plans that make it easier to get quality health care when you need it.

Here are the three things you need to know.

1. Health Insurance Unlocks More Care (and Some of It’s Free!)

When the Affordable Care Act passed in 2010, it set into place several regulations regarding how people apply for health insurance, what services health plans must cover, and more. These regulations affect AI/ANs, too!

Depending on your eligibility, you likely get access to free or low-cost health insurance. These plans are legally required to help pay for certain medical costs, like hospital stays and maternity care, while also offering free preventive services that help you diagnose, prevent, and/or manage health conditions.

And don’t worry: if you sign up for your own health plan, you can still get free care from I/T/Us. If you’re ready to check out plans now, enter your Zip Code below.

2. Your Tribe Membership Affects Your Eligibility

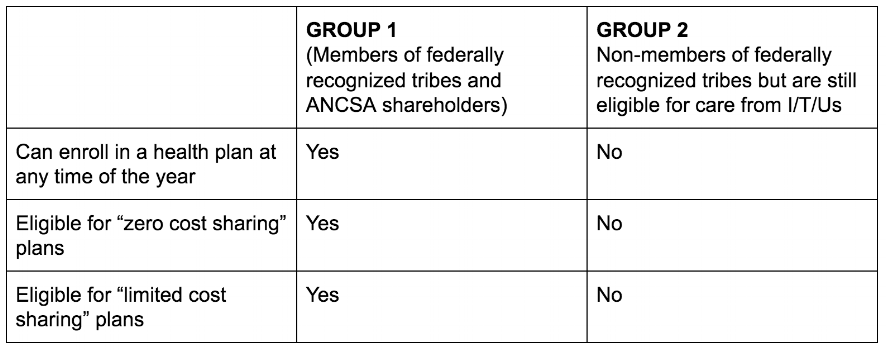

Your eligibility for different government protections depends on your tribe membership. To access your health care benefits, you must first determine which group you belong to:

If you’re not familiar with these acronyms, here’s what they mean:

ANCSA: Alaska Native Claims Settlement Act

I/T/U: Includes the Indian Health Service (IHS), Tribes (or tribal organizations) with an IHS program, and urban Indian health organizations

3. You Could Receive Health Care Benefits Uniquely Designed for AI/ANs

People in Group 1 can receive more perks than those in Group 2, so knowing where you stand is critical.

Group 1

Are you a member of a federally recognized tribe or an ANCSA shareholder? You get access to a wide range of benefits. These include:

Year-round enrollment. Most Americans can enroll for health care only during the Open Enrollment Period, but you can sign up for a plan any time of the year.

“Zero cost sharing” plans. If your income is between 100% and 300% of the Federal Poverty Line (around $12,880 - $38,640 for an individual in most US states), you may be eligible to enroll in a “zero cost sharing” plan. This type of plan doesn’t bill you for any out-of-pocket costs–like deductibles or copays–when you receive care from an I/T/U or receive care that is considered an Essential Health Benefit (EHB). If you receive care that falls under the EHB realm through a provider outside of an I/T/U, you don’t need a referral to avoid paying out-of-pocket costs.

“Limited cost sharing” plans. If your income falls outside the 100 to 300% range, you can enroll in a “limited cost sharing” plan. This means you won’t have to pay any out-of-pocket costs—like deductibles or copays—when receiving care from an I/T/U. To avoid paying out-of-pockets costs when receiving care that is considered an EHB from a provider outside of an I/T/U, be sure to get a referral from your I/T/U provider first.

Group 2

Not a member of a federally recognized tribe? The government still offers certain protections to all AI/ANs eligible to receive care from I/T/Us, including:

No tax penalty. As long as you file for an exemption, you will not have to pay the tax penalty that others are fined for not having health insurance (note: this penalty is now gone in most states).

Easier Medicaid and CHIP eligibility. Medicaid and the Children's Health Insurance Program (CHIP) provide medical coverage without monthly premiums or cost-sharing to people with lower incomes. When determining your eligibility, these services do not count certain sources of income—like payments from Indian trust land, money from selling culturally significant items (like jewelry), and more. This could mean you’re more likely to qualify.

Here’s your benefits quick guide:

Ready to Shop for a Health Plan?

To see available plan options in your zip code, just head to Stride and answer a few quick questions. Be sure to enter your income amount, as that determines plan prices. While we currently do not have enough data to perfectly predict AI/AN subsidy amounts, we can give you an estimate to help compare plan options. And once you select a plan you like, we’ll submit your application through government exchanges to ensure you get the correct subsidy amount. Start by entering your Zip Code below.

Not a member of a federally recognized tribe? We suggest that you check your Medicaid/CHIP eligibility to see if you could receive access to free or low-cost care. If you’re eligible, apply through your state Medicaid agency.

We know this is a lot of information and that it can get confusing fast! If you have any questions about plan eligibility, income estimation, benefits, and more, we have a team of licensed specialists waiting to help. Email us with all your questions support@stridehealth.com.