Can I Use My Health Insurance Out of State?

With summer just around the corner, chances are you’re making plans to head out-of-state on vacation... but don’t hit the road just yet! You need to know how your health insurance will work when you’re out of town.

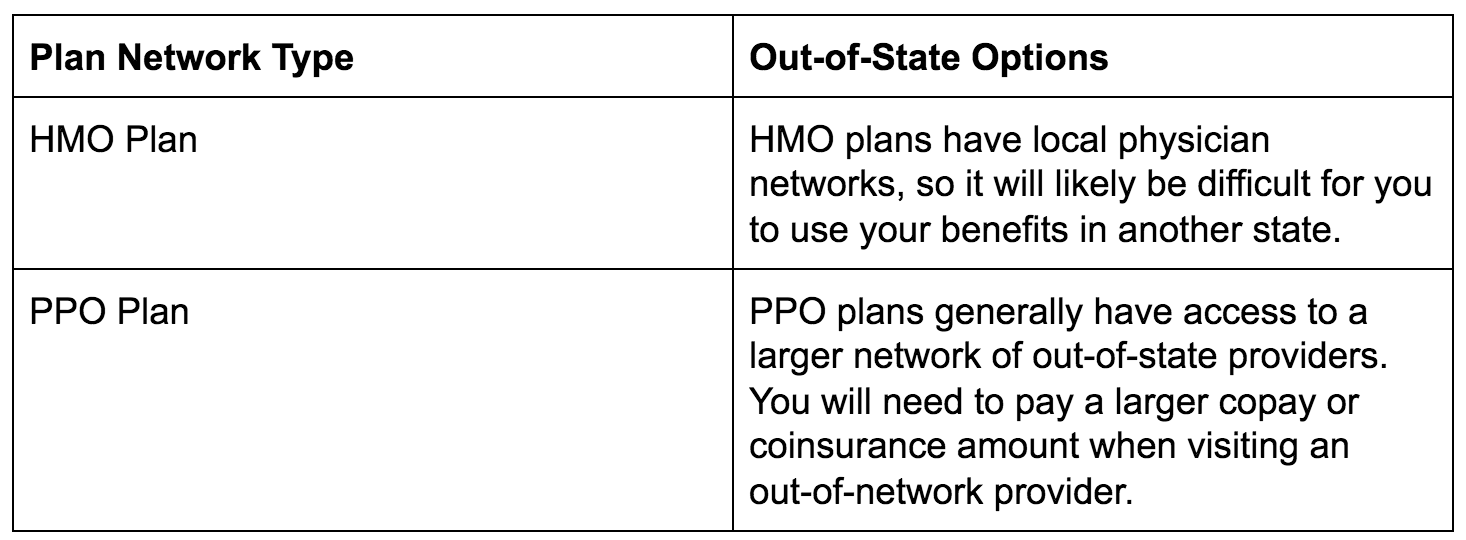

How Insurance Works Out of State

Every insurer negotiates discounted prices with a network of healthcare providers. When you are treated by someone in this group, you receive in-network care, and your insurance will help pay the bill. On the other hand, out-of-network care is not normally covered (or only partially covered) by insurers.

Because insurers negotiate costs on a state-by-state basis, most care away from home is considered out-of-network. How you’ll be billed depends on your plan, but here are the basics:

Life-threatening emergencies are covered. Emergency services are covered in every state. If you have a life-threatening emergency, your hospital care will be billed as in-network. For example, if you get in a car accident and an ambulance takes you to a hospital that doesn’t normally accept your insurance, you’ll still be billed as if you were treated at an in-network facility.

Routine care is NOT always covered. Depending on your network type, your insurance plan may not cover non-emergency care, like doctor checkups, if it is out-of-state.

Generally, PPOs cover you better when you travel out of state. But they also tend to cost more. Depending on how much you use your insurance and how much you travel, an HMO might still be the right choice for you.

Want to compare 2022 health plans and how they might cover you while traveling? Enter your zip code below.

Get to Know Your Insurance Plan

Before you travel, spend some time reviewing your health plan’s Summary of Benefits and Coverage (SBC). This is a document that shows what types of services your plan includes, what percentage you’ll pay for different types of care, and how you’ll be covered in an emergency. You can find an SBC by Googling “[Plan Name + Year] SBC.”

Once you find your SBC, be sure to check how your insurance company defines an emergency. Oscar Health, for example, defines an emergency as something that:

Puts your life in serious danger (like a heart attack or head trauma)

Puts your baby’s life in serious danger, if you’re expecting

Puts yourself or others in serious danger due to a behavioral condition (like depression or schizophrenia)

Impairs how your body functions (for example, you lose a finger or have a stroke).

Seriously disfigures yourself (for example, you break your nose or have second-degree burns).

Keep in mind that you’re only covered until you’re stable; you’ll need to be in-network for your insurance to cover continued services, even if they’re related to your emergency (e.g. follow-up appointments or physical therapy).

Travel Insurance Tips

Always have your insurance card on hand. This provides important plan details, as well as your insurer’s contact information, if you have questions about medical care while you travel.

Inside tip → Keep a photo of your insurance card on your phone!

Look into travel insurance. If after reviewing your SBC you feel like your plan doesn’t provide the best out-of-state coverage, you can always purchase travel medical insurance. These plans will help pay for unexpected medical or dental bills while you’re on the road.

If it’s not an emergency, go to urgent care. If you’re in a life-threatening emergency, dial 9-1-1. But if you need to treat a wound, broken bone, case of the flu, UTI, or other non-emergency issue, find an urgent care facility. These locations are typically half as expensive as ER visits; on average, an out-of-pocket visit to urgent care is only $150. Plus, urgent cares typically get you in and out (and back to vacation!) much faster than the ER.

Have questions about your insurance plan? Send it on over to our team of licensed experts.

Need a health plan that helps cover you when you travel out of state? Start shopping around for 2022 health plans by entering your zip code below.